SRS or CPF: Where should your spare dollar go?

Straight to your inbox. Money, career and life hacks to help young adults stay ahead.

[SINGAPORE] Come next Wednesday (Jul 1), Singapore’s statutory retirement age will be raised from 63 to 64.

If you just started working, this may sound like another piece of skippable news. Chances are, retirement isn’t on the cards for you anytime soon.

But this change could matter more than you think, especially if you haven’t made your first contribution to a Supplementary Retirement Scheme (SRS) account.

Here is the short version: Make a first SRS contribution by Jun 30, even if it’s just S$1, and you can preserve the option to start penalty-free withdrawals from age 63. Wait until Jul 1 or later, and that age becomes 64.

That is because your SRS withdrawal age is tied to the statutory retirement age when you make your first contribution.

Still, you shouldn’t rush to put a large sum into SRS just for the deadline, because the money is meant for retirement and there will be withdrawal restrictions. First, decide whether it suits your finances.

CPF vs SRS: What happens when you top up?

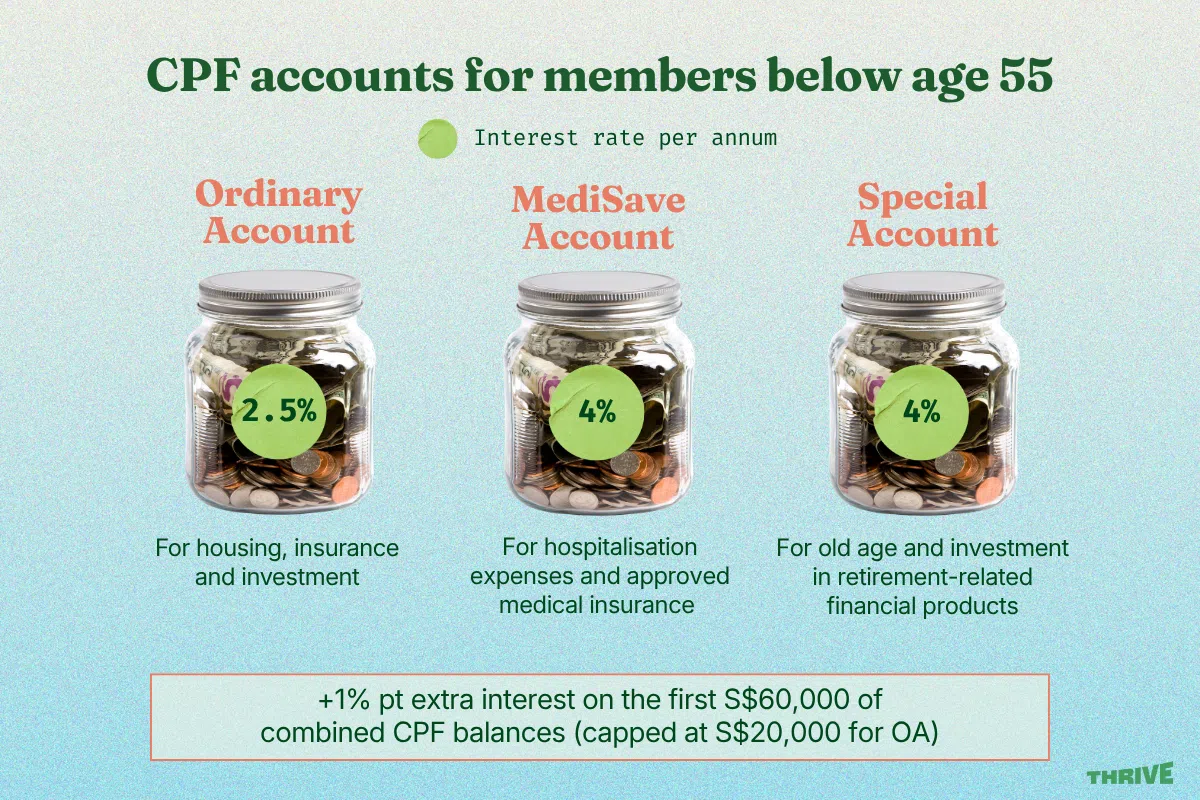

When it comes to government savings schemes, most are probably familiar with the Central Provident Fund (CPF) – the mandatory national savings plan where part of your salary goes towards retirement, health care and housing.

But beyond regular salary contributions, you can also make voluntary CPF top-ups. For younger workers, this typically means topping up the Special Account (SA).

The appeal is that the SA offers relatively high, low-risk interest rates. Eligible cash top-ups also give a dollar-for-dollar tax relief, capped at S$8,000 a year for top-ups to your own account.

The trade-off is liquidity. Once money goes into CPF, it is difficult to withdraw until you’re 55 – and even then there are restrictions depending on whether you have hit the required retirement sums.

The SRS works differently.

Unlike CPF, the SRS is entirely voluntary. Singaporeans and permanent residents can contribute up to S$15,300 each year to their SRS accounts.

Its biggest draw is tax relief. Every dollar you contribute to your SRS account reduces your taxable income by a dollar. CPF and SRS tax reliefs both count towards the overall personal income tax relief cap of S$80,000 that can be claimed each year.

Tax reliefs becomes more useful as your income grows and you rise into higher tax brackets.

However, cash left idle in an SRS account earns only 0.05 per cent interest a year. These funds can instead be invested in a range of products, including stocks, ETFs, unit trusts, bonds and fixed deposits. Any accumulated returns go back into your SRS account and do not count towards the contribution cap.

SRS funds can be withdrawn early, but you’ll have to pay a 5 per cent penalty, and the full withdrawal amount is taxed as income that year.

That is why the Jul 1 change matters. If you withdraw after the statutory retirement age that applied when you made your first contribution, there is no penalty, and only half the withdrawal is taxable.

The idea is that by the time you’re withdrawing your SRS funds, you won’t be earning a salary and hence the tax you pay on your SRS withdrawals will be little to none.

Where should your dollar go?

Ma Xiaoqing, a certified advanced financial planner at Unicorn Financial Solutions, says whether you choose to top-up your CPF or SRS depends on what you value more – liquidity and investment flexibility, or risk-free interest.

For example, one of her clients – an IT worker in his early 30s – chose to top-up his SRS because he wanted more freedom to invest those funds and the option to withdraw early – even if it meant paying a penalty.

While CPF funds can also be invested, there are more restrictions on which investment products are eligible and how much of your total balance you can use.

A new CPF life-cycle investment option is also slated to launch in 2028, offering simplified, low-cost and diversified products for long-term investors. However, details such as selected providers and product offerings have yet to be finalised.

For people who value certainty, Ma says topping up their CPF SA may be the better option, given the risk-free 4 to 5 per cent interest rate. In contrast, idle funds in the SRS that are not invested earn just 0.05 per cent a year.

Still, she stresses that CPF top-ups are irreversible and that young workers should top up only money they are sure they will not need in the near term.

Lorna Tan, head of financial planning literacy at DBS, says that tax savings from contributing to the SRS only become more meaningful at higher income levels.

That’s because Singapore’s personal income tax system is progressive. For the first S$40,000 of your annual chargeable income, the gross tax payable is S$550. For the next S$40,000, the tax payable is S$2,800. For the following S$40,000, it jumps again to S$4,600.

Some people may find the SRS worthwhile at the S$40,000 mark, others at the S$80,000 mark. “But it’s up to you to decide when’s a good time,” says Tan.

In any case, the experts suggest opening your SRS account with S$1 first and anchor that penalty-free withdrawal age, even if you’re not planning to contribute to it soon.

“One year may not seem like a huge difference, but the statutory retirement age will keep increasing,” Ma says.

“So it’s not so much about the one year, but the action of taking ownership in building wealth for the long-term.”

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.