🏛️ Budget cheat sheet so that you can sound smart in office

- Find out more and sign up for Thrive at bt.sg/thrive

📢 Announcements that matter

To preface, this won’t be a cheat sheet of ALL of the new government measures announced in Budget 2024 and how much money we will be getting. There are plenty of resources for that online, and we’ve done a CliffsNotes summary on Instagram as well.

Instead, we want to zoom in on a few announcements and contextualise what they mean while also providing some steps you can take to further your career, homeownership and retirement goals.

Got a diploma? Here’s S$15,000

Graduates from the Institute of Technical Education (ITE) will get financial incentives to further their education.

Upon enrolling in a diploma programme, they will receive a S$5,000 top-up into their Post-Secondary Education Account. Funds in this account can be used to pay for most of the diploma courses offered by ITE and polytechnics here, so the top-up essentially pays for one-and-a-half years’ worth of tuition fees for Singaporeans.

Once these students receive their diplomas, they will get a further S$10,000 top-up to their Central Provident Fund (CPF) Ordinary Account (OA), which will give them a head start in buying a home or saving for retirement.

What this means: Over the past year, the government has been expanding educational pathways for ITE graduates. Last year, the Ministry of Education announced that ITE students who attain a grade point average of 3.5 or higher out of 4 in their Higher Nitec qualifications will be guaranteed admission to a related polytechnic course.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

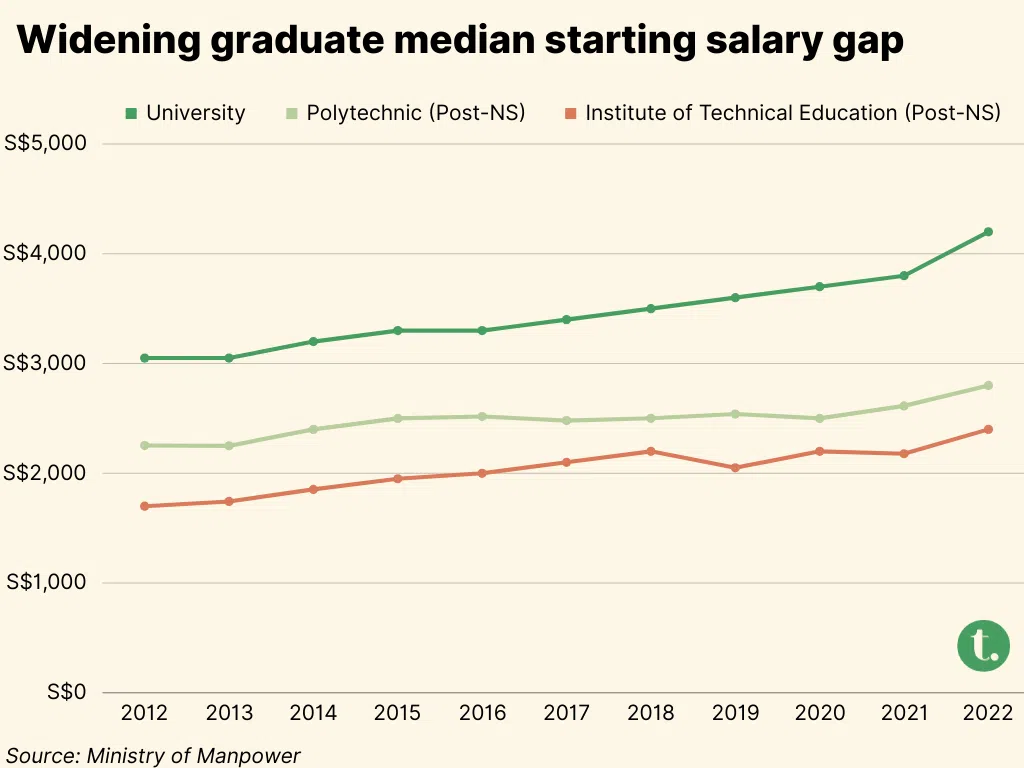

These changes come as the salary gap between university, polytechnic and ITE grads is widening. Today, the median starting salary of a university graduate is about twice that of an ITE graduate.

Hot sectors

During each Budget speech, the finance minister often announces investments in certain areas or industries to further Singapore’s competitiveness. In recent Budgets, these have typically been investments into productivity as well as research and development.

This Budget, Wong said the government will pump more than S$1 billion into AI-related projects over the next five years and provide a S$2 billion top-up to the Financial Sector Development Fund (FSDF), which is aimed at upgrading and developing the financial services sector.

What this means: To borrow a popular idiom and twist it out of context – when in doubt, follow the money. With money flowing in, companies in these two sectors can grow and will likely start hiring more. So, for people thinking of a job switch, these could be two industries to watch. In fact, part of these funds will be going into training talent to take up new jobs that will emerge in the AI and financial services sectors.

Under Singapore’s National AI Strategy 2.0, the government is aiming to triple the number of AI practitioners here to 15,000 by training locals and hiring from overseas. The FSDF provides funding to train people, including polytechnic students and fresh graduates, to work in the finance industry.

CPF changes

Plenty of changes on this front that could make you rethink your retirement strategy.

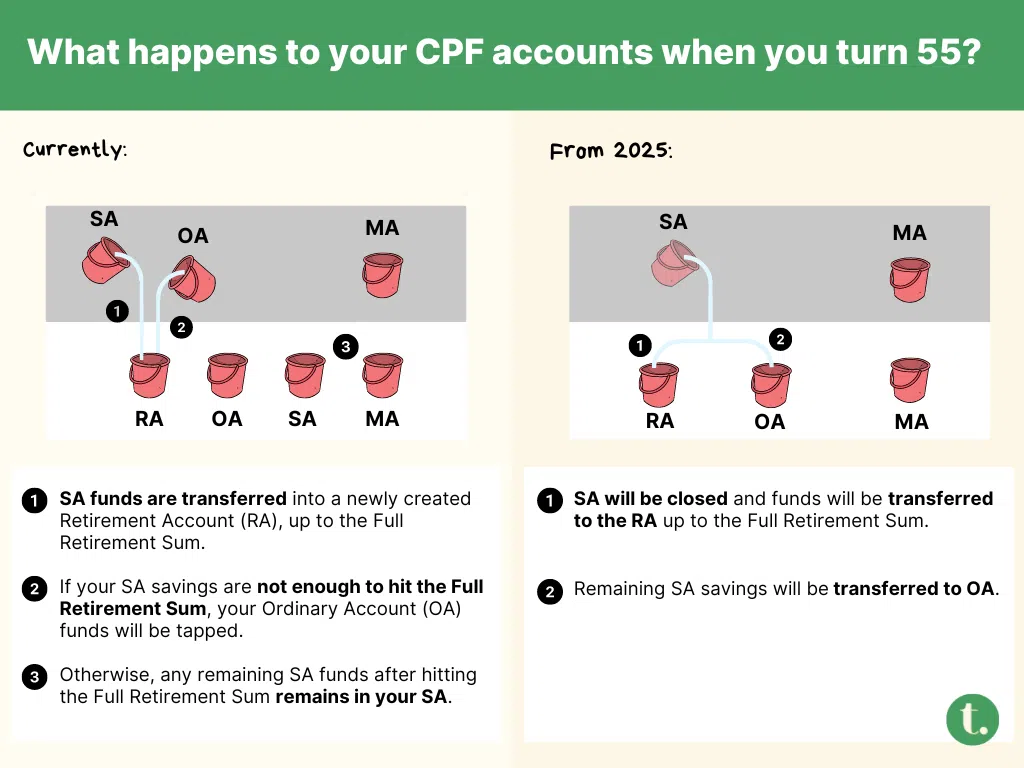

1. From next year, your CPF Special Accounts (SA) will automatically close when you turn 55.

2. The Enhanced Retirement Sum (ERS), which is the maximum savings that can be set aside in the RA, will be raised to four times the Basic Retirement Sum, up from three times. That means the ERS will be S$426,000 in 2025, up from S$308,700 in 2024.

What this means: This could mean you will earn lower interest rates on your remaining SA funds that exceed the Full Retirement Sum since these will flow to the lower-yielding OA, which earns 2.5 per cent per year compared with the SA’s 4.08 per cent interest rate.

That’s unless you choose to voluntarily transfer your OA balance into the RA, which also has an interest rate of 4.08 per cent.

The closure of the SA also gets rid of a little-known “shielding” hack that allowed some savvy CPF members to maximise their interest earnings.

What they did was to “shield” the bulk of their SA savings by investing them a few weeks before their 55th birthday, only to sell the investments off afterwards so that the money flows back to their SA.

That way, their OA balance will be used to fund their RA, and they get to keep their money in their higher-earning SA. 3. From 2025, cash top-ups that attract the Matched Retirement Savings Scheme will no longer grant income tax relief. This scheme provides dollar-for-dollar matching grants for senior Singaporeans who have yet to meet the Basic Retirement Sum.

What this means: If your parents or grandparents have yet to hit the Basic Retirement Sum, you will no longer enjoy tax relief for the first S$2,000 that you top up to their RA. You can still get up to S$8,000 in tax relief for subsequent top-ups to their RA.

That said, if you’re providing for your loved one’s retirement, it still makes financial sense to continue doing so even without the relief. Let’s say you need to contribute S$4,000 to your mom’s retirement pot each year. You can top up S$2,000 to her CPF, and the government will match the other S$2,000, versus giving her S$4,000 in cash.

*Bear in mind that the cap on the matching grant is up to S$2,000 a year, with a lifetime cap of S$20,000

Renting a flat while waiting for your BTO

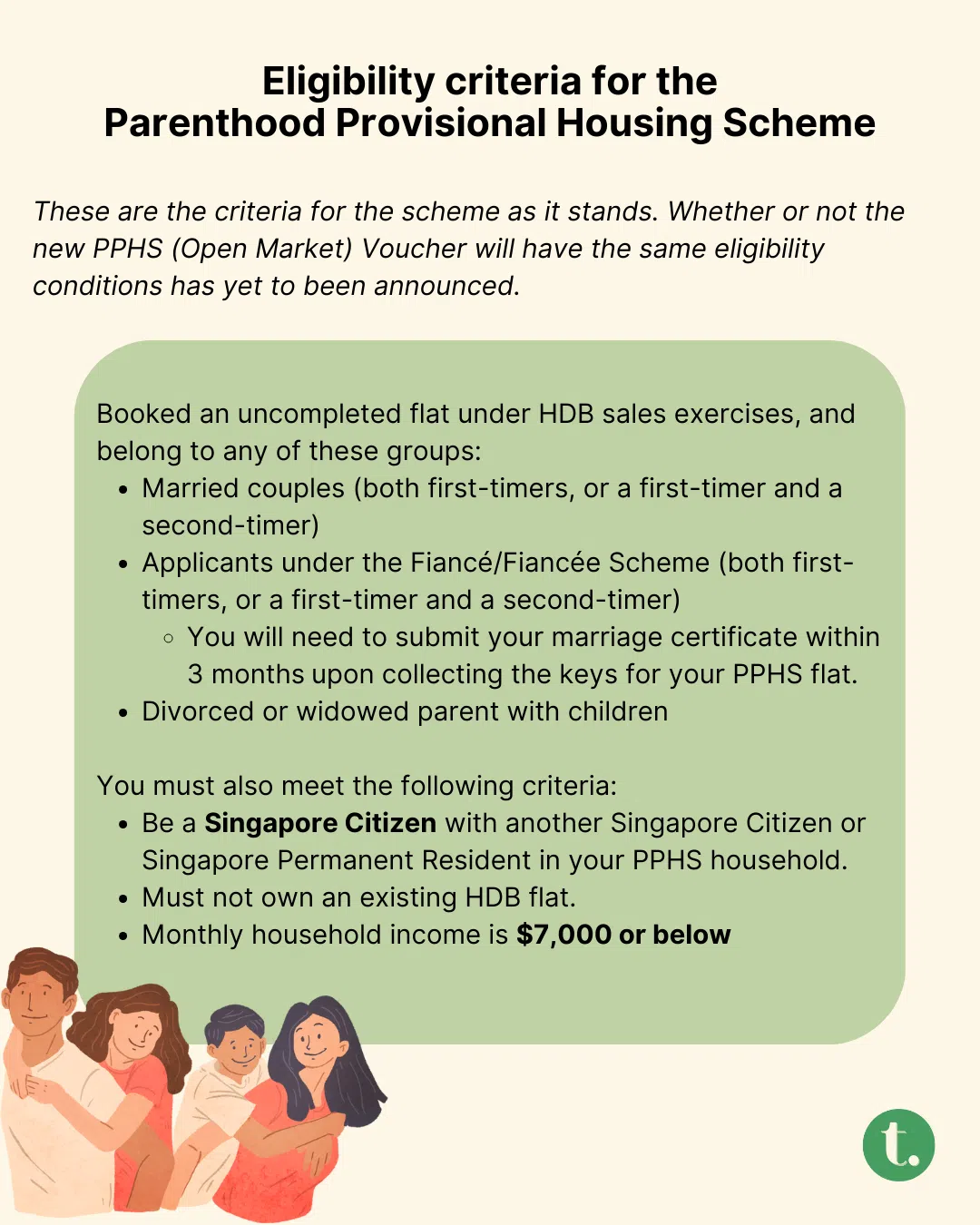

Eligible young families who require housing while waiting for their Build-To-Order (BTO) flats will get further assistance in the form of a one-year rental voucher under the Parenthood Provisional Housing Scheme (PPHS).

What this means: We don’t yet know the dollar amount of this voucher, but we know that it is meant to allow eligible families to rent an HDB flat in the open market.

The Housing and Development Board (HDB) currently offers subsidised housing under the PPHS. Rentals for two-room flats are between S$400 and S$550, and three-room flats are between S$600 and S$900.

As it stands, the PPHS is available only to couples with a monthly household income of S$7,000 or below. These rentals are highly sought after, and married couples with a child are given priority, so the vouchers could help alleviate the high demand.

Already, some property experts and agents are worried that landlords will start charging higher for rent, knowing that tenants have vouchers to use. But we’ll have to wait for the details of the voucher and its eligibility criteria to get greater clarity on the scheme’s impact.

TL;DR

- ITE grads will have more reasons to take up a diploma

- The AI and financial services sector could be one to watch if you’re looking for a job

- Topping up your parents’ CPF accounts will no longer grant you tax relief if they attract the government’s matching grant

- More young couples will get help renting a flat while waiting for their BTOs

Copyright SPH Media. All rights reserved.

DeeperDive is a beta AI feature. Refer to full articles for the facts.

TRENDING NOW

‘Boring’ is the new black: The stars are aligning for a Singapore stock market revival

Near sell-out launches in March boost developer sales to 1,300 units after four slow months

China pips the US if Asean is forced to choose, but analysts warn against reading it like a sports result

Genting Singapore’s Lim Kok Thay receives S$7.5 million pay package for FY2025