SIA H2 FY2026 earnings fall 53.6% to S$945.5 million on absence of accounting gain

SIA’s share of Air India’s full-year losses mounts to S$945.2 million

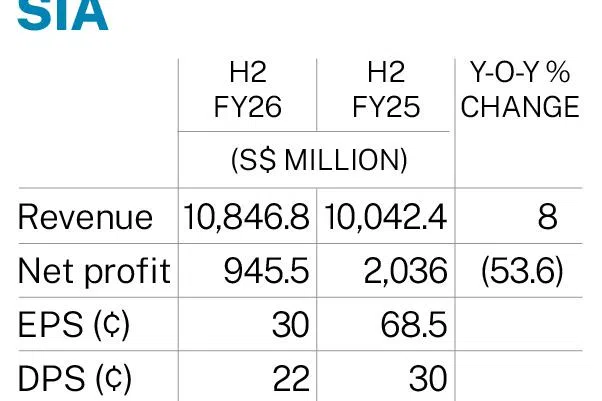

[SINGAPORE] Singapore Airlines’ (SIA) earnings for its second half ended March more than halved year on year (yoy) to S$945.5 million from S$2 billion.

The national carrier group on Thursday (May 14) attributed the 53.6 per cent reduction in H2 net profit largely to the absence of a one-off, non-cash accounting gain of S$1.1 billion. This was from the disposal of Vistara airline and recognised in the year-ago period.

However, SIA posted a record revenue of S$10.8 billion for H2 FY2026, up 8 per cent yoy. At the operating level, the group’s profit also hit a high of S$1.6 billion, jumping 72 per cent.

Its passenger flown revenue rose 8.5 per cent, driven by 3.8 per cent stronger yields and 4.7 per cent higher passenger traffic.

Cargo flown revenue dipped 1.3 per cent on weaker yields, which declined 3.5 per cent.

Group expenditure increased 1.6 per cent, on higher non-fuel expenditure climbing 5 per cent.

The rise in non-fuel expenditure was due mainly to capacity increase and higher cost pressures. It was partly offset by a decline in net fuel cost, which was a result of the swing from a fuel hedging loss in FY2025 to a gain in FY2026.

Earnings per share for H2 FY2026 also more than halved to S$0.30, from S$0.685 previously.

Net asset value per share was S$5.48 as at Mar 31, versus S$5.27 in the year-ago period.

SEE ALSO

The board recommended a final ordinary dividend of S$0.22 per share for FY2026.

SIA had earlier paid an interim dividend of S$0.05 a share for H1 FY2026 ended September. It also proposed a special dividend package of S$0.10 per share annually over three financial years.

In total, the ordinary and special dividend for FY2026 stood at S$0.37 a share.

The full-service airline is rewarding eligible employees with a profit-sharing bonus of 5.7 months for FY2026, The Business Times has learnt.

For the full year, the airline group’s net profit declined by 57.4 per cent to S$1.2 billion. This was also primarily due to the absence of the non-cash accounting gain from the completion of the Air India-Vistara merger.

The swing from a share of profits of associated companies in FY2025 to a loss in FY2026 was because SIA accounted for its share of Air India’s full-year losses that mounted to S$945.2 million. In contrast, the group considered only four months in the previous year.

SIA holds a 25.1 per cent stake in the Indian joint venture airline.

As at Mar 31, the airline group’s carrying amount in Air India amounted to S$1.1 billion against a total cost of S$2.1 billion. SIA’s management assessed that there were indicators of impairment for the investment in Air India, triggered by challenging operating conditions and heightened geopolitical uncertainty.

The SIA group’s full-year revenue rose 5 per cent on the year to a peak of S$20.5 billion. It also carried a record 42.4 million passengers, up 8 per cent yoy.

Full-year operating profit expanded 39 per cent to S$2.4 billion.

Jet fuel price impact to come

SIA said the full impact of higher jet fuel prices is expected to feed through in FY2027, as the surge was only partially reflected in the net fuel cost for March due to pricing lags.

Jet fuel, which is the single largest expenditure item for airlines including the SIA group, has more than doubled in price since the US and Israel attacked Iran on Feb 28.

SIA and Scoot have since raised airfares across their networks, but the group said these adjustments do not fully offset the spike in jet fuel prices.

The group manages cost volatility through risk management, including fuel hedging.

Cost pressures are mounting as suppliers increase prices amid higher energy expenses and disrupted supply chains. This high-inflation operating environment is likely to persist, SIA said.

Depending on the duration of the Middle East conflict and how the situation evolves, there could be broader implications for supply chains and macroeconomic conditions, affecting demand.

But SIA noted that it has clinched opportunities from the shifts, such as adjusted frequencies and capacity, to capture demand to Europe and Australia.

The group’s passenger network served 134 destinations in 35 countries and territories as at Mar 31, with the full-service airline serving 77 destinations and Scoot, 82.

The cargo network comprised 137 destinations in 36 countries and territories.

As at end-March, the group’s operating fleet had 218 passenger and freighter aircraft.

SIA shares finished 0.2 per cent or S$0.01 lower at S$6.27 on Thursday, before the results were announced.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.

TRENDING NOW

Hong Leong, GuocoLand JV sole bidder for condo plot on former Keppel Club site

Nvidia will soon face a chip limit, warns Huawei’s top scientist

Yeoh Pei Xien: YTL’s third-gen scion with a pastor’s heart

Lower consent hurdle among changes proposed for en bloc sales to spur redevelopment, protect minority owners