Four wild cards stand between Vietnam and its 11.9% H2 growth target

The country is trying to shift into an even higher gear after H1 growth topped 8%

As Vietnam crosses into the World Bank’s upper-middle-income category after what was described as one of the region’s strongest runs of sustained growth, the country now faces a harder test: pushing that momentum even faster.

Growth is already strong, and ahead of most regional peers. But it is still not strong enough for Hanoi’s ambition of achieving double-digit expansion this year and sustaining that pace till 2030.

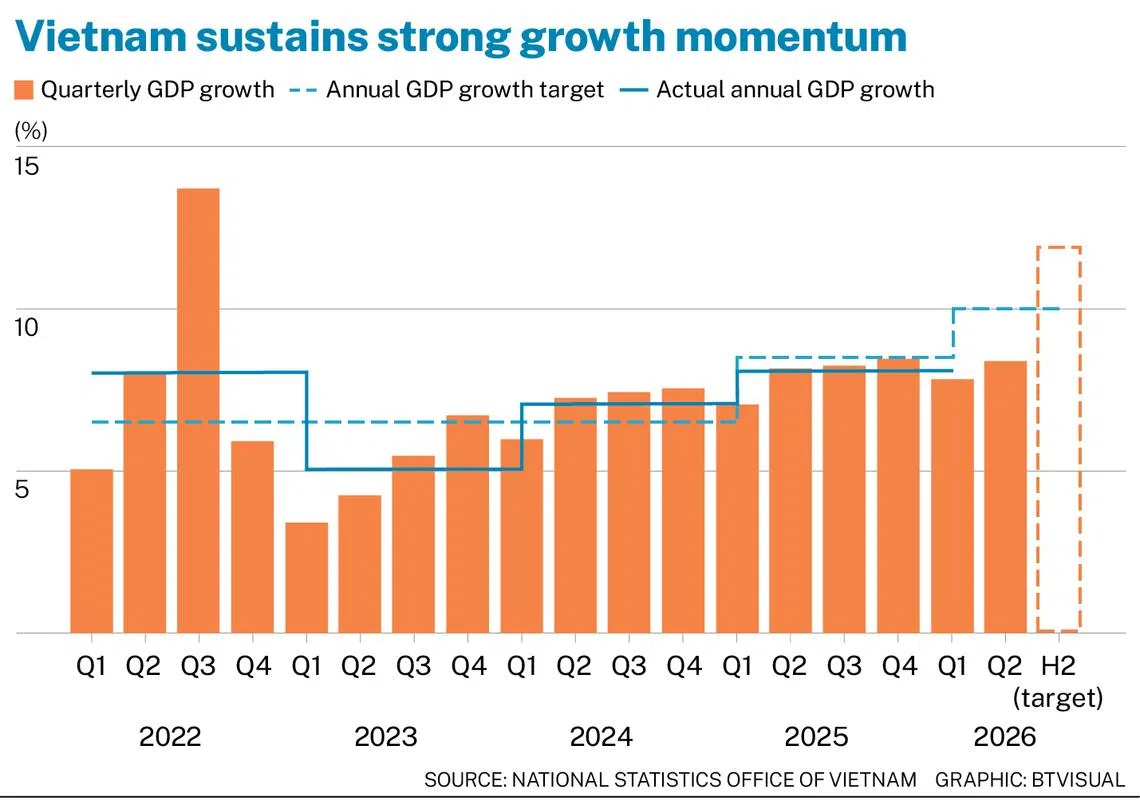

Official data released on Friday (Jul 3) showed that Vietnam’s economy grew 8.39 per cent in the second quarter year on year, accelerating from 7.83 per cent in the first quarter. Growth for the first half came in at 8.18 per cent from a year ago.

That means the second half would have to do much of the heavy lifting – expanding by 11.9 per cent – under stronger government measures laid out in a resolution issued on Jun 27.

Without that acceleration, full-year growth could reach only 8.7 per cent, according to latest projections compiled from ministries and localities – or even come in closer to the World Bank’s more moderate 6.8 per cent forecast.

It is also worth noting that this push comes at a more difficult moment for macroeconomic management. Higher energy costs, a stronger US dollar, trade frictions and inflation pressure narrow the room for Vietnam’s broad-based stimulus.

Here are the four wild cards that will determine whether Vietnam can close the gap in the coming six months.

1. Can public spending deliver fast enough?

The clearest growth lever is state capital spending. The government’s revised financial strategy for 2026-2030 targets development investment spending at around 40 per cent of total state expenditure, compared with about 28 per cent in the previous period.

More than 8.2 quadrillion dong (US$311.8 billion) will be allocated for public investment in the period, about 2.7 times the implementation level in previous five years.

SEE ALSO

The budget for 2026 alone is 1.08 quadrillion dong, the largest on record and roughly 175 trillion dong higher than what was planned for 2025.

However, actual spending tends to lag, with calendar-year disbursement having repeatedly fallen short of annual plans. As at Jun 26, nearly 300 trillion dong had been disbursed, equivalent to only about 29 per cent of the full-year target, the Ministry of Finance indicated.

Bottlenecks include slow land clearance, shortages of construction materials, higher input prices, incomplete investment procedures and weak project preparation.

Ministries, agencies and localities are now required to fully disburse their 2026 public-investment allocations, with weekly, monthly and quarterly schedules to identify delays and strengthen accountability.

In its investment strategy report for the second half, VNDirect Research said that it expected a wave of major infrastructure projects to be completed or launched in the final six months of the year, with the combination of public investment and public-private partnerships (PPP) providing “a strong push”.

The brokerage noted: “The PPP model is being promoted to mobilise private-sector resources, thereby accelerating construction progress and improving capital efficiency.”

2. Can credit expand without destabilising risks?

Bank credit remains central to Vietnam’s growth model, but the latest policy moves point to a targeted loosening rather than a broad-based credit boom.

The measures include raising the cap on short-term funding that banks can use for medium and long-term lending, adding flexibility to the use of idle State Treasury funds to support banking-system liquidity, and carving out selected sectors and nationally important projects from ordinary lending limits.

Credit was already supporting economic activity in the first half. By Jun 26, total outstanding credit across the banking system exceeded 19.97 quadrillion dong, up 7.41 per cent from the end of 2025 and 18.1 per cent from a year earlier.

The central bank had earlier set systemwide credit growth at around 15 per cent for the full year, leaving some room to support the economy through the rest of 2026.

But that does not mean prudential concerns, inflation and currency risks can be ignored, especially if an aggressive US Federal Reserve rate-hike cycle weakens the dong and tightens domestic financial conditions further.

3. Can foreign capital do the harder job?

Bank credit remains the main source of capital for the economy, but the scale of infrastructure, private investment and corporate expansion needed to sustain faster growth requires deeper capital markets and more external funding.

That is why the government is trying to widen the country’s financing channels – not only through stock-market reforms, larger foreign loans and official development assistance, but also by attracting foreign direct investment (FDI) in higher-value sectors.

FDI remains the strongest part of the foreign-funding picture. In the first half of 2026, registered foreign investment reached US$34.65 billion, up 61 per cent year on year, while disbursed FDI rose 11.2 per cent to US$13.03 billion, the highest first-half implementation level in at least 18 years.

A Politburo resolution dated Jun 8 also sets a new direction for the foreign-invested sector. It prioritised high-technology, high-value-added investment and stronger domestic linkages.

Analysts at Ho Chi Minh City Securities Corporation said that one of the most significant aspects of the resolution is its emphasis on raising localisation rates to 40 to 50 per cent in key industries.

“This represents a structural shift from the traditional FDI model, where Vietnamese enterprises have largely participated in low-value-added activities such as assembly, while technology transfer and knowledge spillovers remained limited,” they wrote in a note on Jul 1.

4. Can exports outrun trade risks?

Vietnam’s export engine is still running in the first half, with exports rising 21 per cent year on year to US$266.5 billion. It was helped by strong global demand for electronics and artificial intelligence-related supply chains.

Imports, however, grew faster, up 33.4 per cent to US$283.2 billion. Six straight months of trade deficits have then pushed the cumulative shortfall to a record high of nearly US$17 billion, reversing a US$7.63 billion surplus a year earlier.

Still, Maybank economists Brian Lee Shun Rong and Chua Hak Bin said that the widening trade deficit is unlikely to weigh on real GDP growth.

They noted that an increase in intermediate input imports is taking place “as manufacturers ramp up investments, which will support the export growth momentum”.

Companies formed with foreign investment remain the backbone of Vietnam’s export machine, accounting for around 80 per cent of total export turnover.

VinaCapital economist Michael Kokalari also pointed out in June that FDI companies – especially Chinese high-tech ones – were increasingly importing capital goods used in the production of precision components in Vietnam.

That investment cycle is unfolding even when Vietnam’s external risks are rising. The country stands out as the only Asean economy facing three active US investigations, covering alleged excess manufacturing capacity, forced-labour enforcement and intellectual-property protection.

“The investigations could yield higher US tariffs than on its peers, although present exemptions, such as electronics, will likely be maintained,” the Maybank economists added.

Some analysts, meanwhile, see the trade risk as manageable. “As long as tariffs on Vietnam’s exports to the US are not more than 10 percentage points above those imposed on its emerging market competitors, Vietnam’s other advantages, such as low wages, will more than offset the additional US tariffs,” Kokalari added. THE BUSINESS TIMES

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Share with us your feedback on BT's products and services

TRENDING NOW

ABSD deadline extended to up to 7 years for developers of large en bloc sites to encourage reuse of land

15-month wait-out curb lifted for private property owners buying HDB resale flats

Mortgagee-sale listings hit six-year high in H1 2026 as financing conditions tighten

Knight Frank winds down real estate agency unit, agents to move to OrangeTee & Tie