Singapore core inflation cools to 1.4% in April in benign surprise

The headline figure holds steady at 1.8%

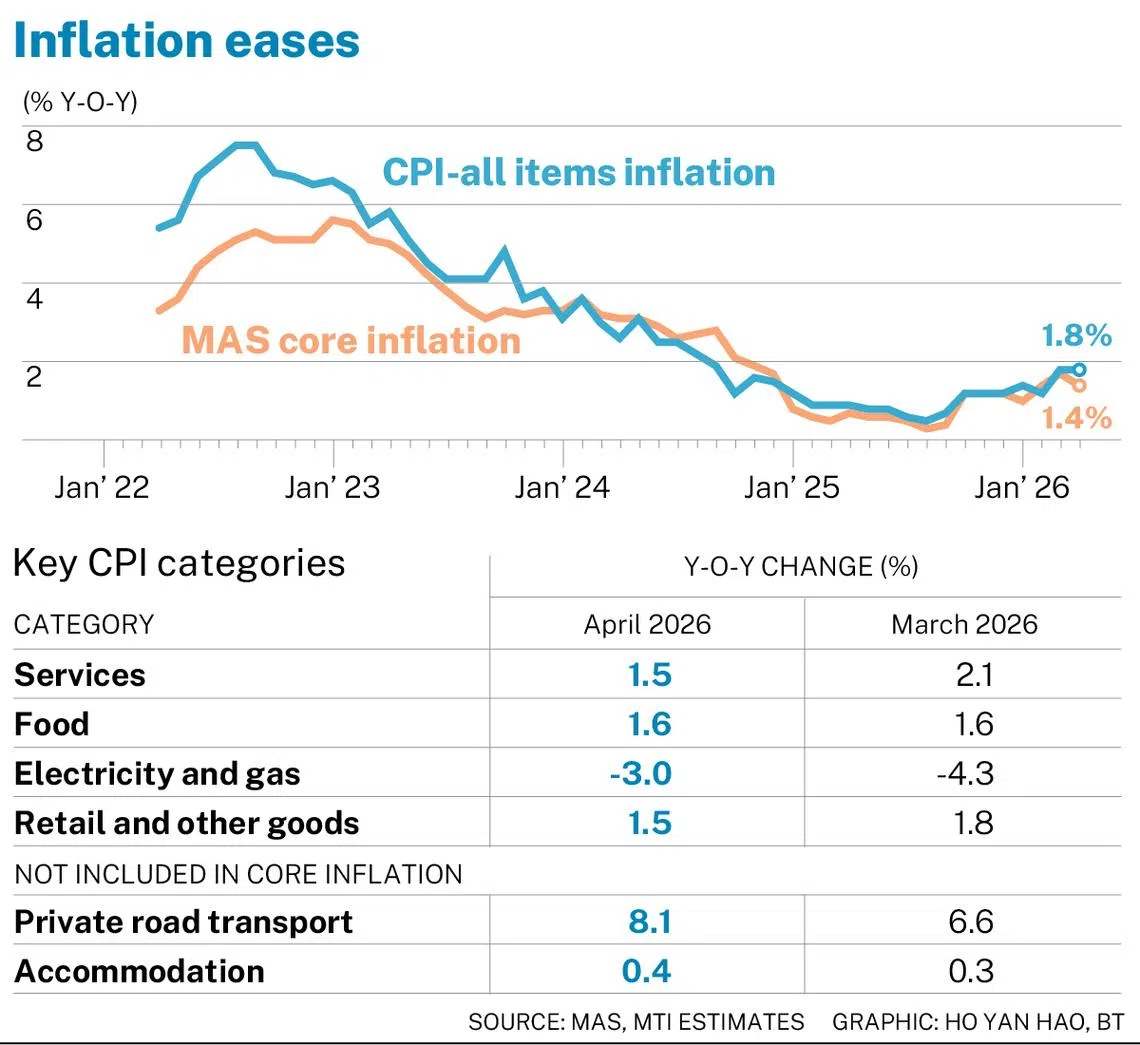

[SINGAPORE] The Republic’s core inflation eased to 1.4 per cent in April from 1.7 per cent in March, defying economists’ expectations.

The Monetary Authority of Singapore (MAS) and the Ministry of Trade and Industry (MTI) said in a statement on Monday (May 25) that this was largely due to lower services as well as retail and other goods inflation.

Private-sector economists had expected the rate for core inflation, which excludes accommodation and private transport, to rise to 1.8 per cent, a Bloomberg poll indicated.

Economists attributed the surprise moderation mainly to lower health insurance inflation. This followed the roll-out of new Integrated Shield Plan riders from Apr 1, which resulted in lower premiums.

Data showed that services inflation, which includes healthcare costs, fell to 1.5 per cent in April from 2.1 per cent in March.

Bank of America (BOA) economists Ang Kai Wei and Rahul Bajoria said the decline in insurance premiums was not fully reflected in analysts’ forecasts, while Barclays economist Brian Tan said the drag from the health insurance segment was larger than expected.

However, DBS senior economist Chua Han Teng said the softer reading did not necessarily signal weaker demand conditions, citing the continued resilience of the labour market and broader economy.

Meanwhile, headline inflation held steady at 1.8 per cent in April, as higher private transport and accommodation inflation was offset by lower core inflation.

The reading also came in below economists’ expectations of 2.1 per cent.

On a month-on-month basis, the core consumer price index edged up by 0.2 per cent, while the all-items CPI declined by 0.3 per cent.

Inflation outlook

MAS and MTI adjusted their 2026 full-year forecast range for both core and headline inflation to 1.5 to 2.5 per cent, up from 1 to 2 per cent previously.

Still, they cautioned that Singapore’s imported cost pressures are expected to pick up and broaden in the months ahead.

“As higher energy and other input costs arising from the developments in the Middle East pass through global supply chains, they will raise production and transport costs for a wider range of Singapore’s imported goods and services,” said the authorities.

Therefore, they expect inflation risks to remain tilted to the upside, as more persistent disruptions to global energy supplies or shortages of key intermediate inputs in regional supply chains could further raise imported costs for Singapore.

However, MAS and MTI added that downside risks are also present.

“A curtailment of industrial production due to supply chain disruptions or an abrupt tightening in global financial conditions could lead to a slowdown in economic activity and thus lower inflation,” they said.

Monetary policy

Economists were mixed on the outlook for monetary policy, with some expecting MAS to tighten further later in 2026, and others saying the softer inflation reading supports a pause for now.

BOA, Barclays and RHB Bank expect the central bank to stand pat.

Barclays’ Tan said the downside surprise in core inflation supports the view that MAS is unlikely to make further adjustments to the Singapore dollar nominal effective exchange rate (S$NEER) policy band in the near term, although risks remain tilted towards additional tightening.

In contrast, Maybank expects MAS to tighten policy in July.

Its economists Chua Hak Bin and Brian Lee characterised April’s decline in core inflation as a “temporary blip”, noting that administrative factors had partly contributed to lower health insurance and water price inflation.

They noted that water price inflation eased as the impact of last April’s 10 per cent water tariff hike dissipated.

They added that inflationary pressures from higher energy, shipping and raw material costs have yet to fully feed through to the broader economy, as some businesses may still be absorbing higher costs amid competitive pressures and softer consumer demand.

“Inflationary pressures in a wider range of products are therefore likely to increase in the coming months, as firms in the non-transport and utilities sectors eventually pass on higher input costs to consumers,” the economists said, adding that they expect monthly inflation to overshoot 2 per cent in the second and third quarters.

They therefore predict MAS will steepen the S$NEER policy band slope by another 50 basis points at its July monetary policy meeting, citing resilient growth and upside risks to inflation.

Meanwhile, UOB expects the central bank to tighten policy in October instead. Associate economist Jester Koh said the softer core inflation reading could still strengthen the case for further policy tightening.

He also cited firmer underlying inflation momentum, rising imported inflation and early signs that price pressures are broadening across the economy.

UOB’s view is for MAS to steepen the S$NEER policy band slope by 50 basis points to 1.5 per cent a year in October.

However, there remains a chance of an earlier move in July if higher business costs begin feeding more broadly into consumer prices than expected, Koh said.

He added that more aggressive tightening measures – such as an upward re-centring of the S$NEER policy band – would likely only be considered if MAS becomes convinced that full-year core inflation could rise well above 2.5 per cent.

Key CPI categories

In April, inflation trends across CPI categories were mixed, with private transport and accommodation costs rising faster while retail goods and electricity prices remained subdued.

Private transport recorded the largest increase in inflation, rising to 8.1 per cent year on year in April, from 6.6 per cent the month before, due to steeper increases in petrol and car prices.

Accommodation inflation inched up 0.4 per cent, from 0.3 per cent in March, due to a larger increase in housing rents.

Meanwhile, retail and other goods inflation slowed marginally to 1.5 per cent, from 1.8 per cent in March, as water price inflation eased.

Services inflation likewise fell to 1.5 per cent in April, from 2.1 per cent previously, due to a smaller increase in health insurance costs as well as lower telecommunication services prices.

Electricity and gas prices fell at a slower pace of 3 per cent, compared with a 4.3 per cent decline in March, due to a smaller drop in electricity prices.

As for food inflation, it held steady at 1.6 per cent as the prices of non-cooked food and food services rose at similar rates in April and March.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.