OCBC’s Indonesia deal a ‘perfect fit’ for Asean wealth ambitions, says CEO, as Q1 profit beats estimates

Lender’s earnings for period rise 5% to S$1.97 billion

[SINGAPORE] OCBC’s acquisition of HSBC’s wealth and retail portfolio in Indonesia is a “perfect fit” for the lender’s refreshed growth road map, said group CEO Tan Teck Long on Friday (May 8).

This comes as strong wealth income helped drive a robust first-quarter earnings performance.

“If you recall, under our ‘Next Frontier’ strategy, we said that we are focused on growing wealth, as well as deepening our franchise in our core markets,” said Tan at the bank’s earnings briefing.

“When I looked at (HSBC’s) portfolio, I realised this (acquisition) is a perfect fit,” he added.

The move included doubling down on the bank’s wealth proposition and sharpening its focus on core Asean markets, which includes Indonesia. At an earlier briefing in February, Tan flagged that the lender was exploring merger and acquisition opportunities in the region.

That ambition has since materialised.

On Monday, OCBC announced that its Indonesian subsidiary, Bank OCBC NISP, would acquire HSBC’s retail and wealth management operations in Indonesia.

The consideration will comprise the Indonesian business’ net asset value upon completion, plus a premium of up to 6.5 trillion rupiah (S$475.5 million). The deal is expected to close in the second quarter of 2027.

The acquisition is expected to contribute to earnings and add S$6.6 billion to OCBC Indonesia’s assets under management. This figure includes S$4.3 billion of customers’ investments in mutual funds and bonds, as well as insurance and customer deposits of S$2.3 billion.

SEE ALSO

A retail loan book of S$300 million and about 336,000 customers will also be transferred to OCBC Indonesia. Around 1,300 employees are expected to join its wealth management operations.

Tan described the HSBC portfolio as “very clean”, noting that it is largely made up of deposits and assets under management, unlike “most other” portfolios in the market that tend to comprise a mix of loans and deposits.

Acquiring a portfolio without a significant loan component means the bank does not need to “worry about” credit costs or single-borrower concentration risks, he said.

“What I really like when I look at the deposits part of the acquisition (is that) they have sizeable Casa,” he added, referring to current account and savings account deposits, which provide banks with low-cost funding.

Tan also described the wealth portion of the portfolio as “highly complementary” to OCBC’s existing Indonesian franchise.

“We are one of the top three privately owned banks in Indonesia… we can bolt on this acquisition and gain cost synergies very quickly. Not many banks can match our economies of scale in Indonesia,” he said.

To support its wealth ambitions, OCBC will continue expanding its sales-related wealth headcount, although the bank intends to “maintain high cost discipline” at the group level.

Asked about competition in both mergers and acquisitions and wealth hiring – after reports that DBS and UOB had also bid for the HSBC portfolio and separately spoken about growing their wealth teams – Tan said competition was not new to OCBC.

Still, he noted that the exit of several international players from Asean in recent years has resulted in a less crowded competitive landscape across the region.

Wealth income offsets margin pressure

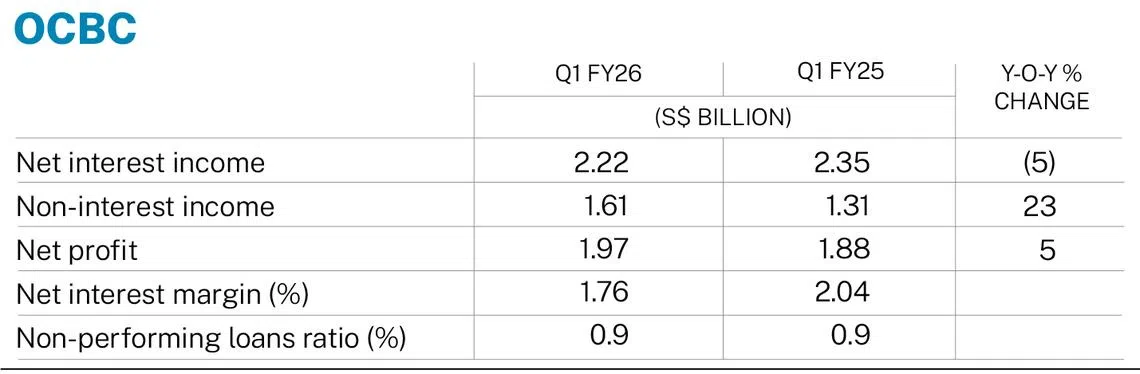

On Friday, OCBC reported a 5 per cent rise in net profit for the first quarter ended Mar 31 to S$1.97 billion, from S$1.88 billion a year earlier.

The result exceeded the S$1.88 billion consensus estimate in a Bloomberg survey.

Net interest income fell 5 per cent to S$2.2 billion amid a lower interest rate environment, as net interest margin narrowed by 28 basis points to 1.76 per cent, from 2.04 per cent previously.

This came as benchmark rates in Singapore and Hong Kong declined year on year by more than 170 and 160 basis points, respectively.

However, the weakness was more than offset by non-interest income, which rose 23 per cent to a record S$1.61 billion.

Under that bucket, wealth management fees climbed 34 per cent to S$422 million, supported by stronger customer activity across all wealth product channels.

The non-performing loan ratio was unchanged at 0.9 per cent.

Total allowances rose 2 per cent to S$216 million, largely due to higher provisions for “third-order” effects from the ongoing Middle East war. These were mainly linked to risks of a macroeconomic slowdown arising from elevated oil and energy prices.

“We note no significant credit deterioration, and continue to refresh our stress tests,” said group chief financial officer Goh Chin Yee at the briefing. “(The) first-order impact is not material, at less than 3 per cent of loans or 1 per cent of total assets.”

Tan added that operations in Dubai – where OCBC’s private banking arm, Bank of Singapore, runs a branch – have not been affected.

Staff there continue to work remotely, including the 10 to 20 per cent of employees who voluntarily chose to leave the country after the outbreak of the war.

The bank maintained its FY2026 guidance, including expectations for total income to remain “stable to growing”, along with a “slight to moderate” decline in full-year net interest income.

The latter outlook assumes one US Federal Reserve rate cut in the fourth quarter of 2026, as well as benchmark Singapore and Hong Kong interest rates of 1.2 per cent and 2.7 per cent per annum, respectively.

OCBC maintained its expectations for mid-single-digit loan growth, credit costs of 25 to 30 basis points, and a cost-to-income ratio in the mid-40 per cent range.

In the first quarter, loans grew 8 per cent year on year to S$347 billion. Credit costs improved by one basis point to 23 basis points, while the cost-to-income ratio rose to 39.3 per cent from 38.7 per cent previously.

OCBC rounded off the first-quarter earnings season for Singapore’s three local banks, following DBS on Apr 30 and UOB on Thursday.

Shares of OCBC rose 0.2 per cent or S$0.04 to close at S$21.92 on Friday, the same day the bank paid out dividends.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.