UOB aims to double wealth income to at least S$2.5 billion by 2030; Q1 profit slips 4%

CEO Wee Ee Cheong says the completion of its Citi integration gives the bank a ‘long runway’ for organic wealth growth across Asean

[SINGAPORE] UOB has set a target of doubling its wealth management income by 2030, as it looks to further expand in the affluent segment across Asean. This “underpenetrated” sector could drive its next phase of growth, said deputy chair and chief executive officer Wee Ee Cheong on Thursday (May 7).

The target will be benchmarked against the figures for the 12 months ended Dec 31, 2025. In FY2025, UOB’s wealth management income rose to S$1.28 billion, from S$1.12 billion the year before.

The latest goal implies that the lender is aiming for a wealth management income of at least S$2.5 billion by 2030, following the completion of its acquisition of Citigroup’s retail banking assets in four Asean markets.

Speaking at the bank’s first-quarter results briefing, Wee said: “Over the past three years, our focus has been on integrating the Citi portfolio and bringing everything into a single, unified platform. That work is largely completed.”

He was referring to UOB’s S$4.9 billion acquisition of Citigroup’s retail banking businesses in Indonesia, Malaysia, Thailand and Vietnam. The deal, announced in 2022 and completed in 2025, doubled UOB’s customer base in those four markets to 8.5 million.

Wee acknowledged that the integration had been “not as straightforward” as initially expected, and that the bank had to continue operating Citi’s platforms while simultaneously building its own systems, a process that cost an “arm and (a) leg”.

However, he added, the integration work has now been completed, with the associated costs already recognised in previous quarters.

Looking ahead, he sees “significant opportunities” in wealth management, supported by “a large and increasingly affluent customer base that is underpenetrated”.

“This gives us a long runway for sustainable, organic growth,” he said.

Investors will begin to see income from the wealth business “picking up” over the coming quarters, he added, as the lender works towards its 2030 target.

To support its wealth ambitions, UOB plans to expand hiring for wealth-related roles such as relationship managers, although overall headcount is expected to remain broadly stable.

On inorganic growth opportunities such as acquisitions, Wee said that the bank is not ruling them out, though valuations are likely to remain “very high”.

“Other people don’t have (our) customer base,” he noted. “I have the customer base – that is a key differentiator.”

His remarks came just days after OCBC announced on Monday that it would acquire HSBC Indonesia’s retail and wealth business, with the transaction expected to close in the second quarter of 2027.

DBS, OCBC and UOB had all reportedly been among the bidders for the business.

Elaborating on UOB’s acquisition strategy, group chief financial officer Leong Yung Chee said that the lender remains “always on the lookout for opportunities, whether previously or going forward”, but added that any deal must “check quite a few boxes”.

These include whether an acquisition brings desired capabilities, fills business or geographical gaps and comes at the “correct” price. Integration costs must also be factored in alongside acquisition costs, Leong added.

Q1 profit slips on lower rates

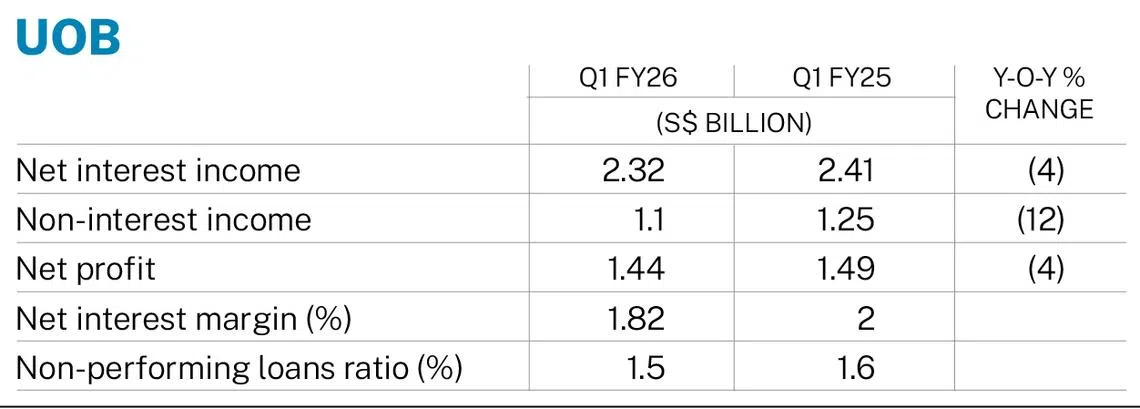

The lender on Thursday reported a 4 per cent decline in net profit to S$1.44 billion for the three months ended Mar 31, 2026, although the results beat the S$1.39 billion consensus estimate in a Bloomberg survey.

Net interest income fell 4 per cent to S$2.32 billion as lower benchmark rates weighed on margins. Net interest margin narrowed by 18 basis points to 1.82 per cent, from 2 per cent in Q1 FY2025, amid lower benchmark rates in Singapore and Hong Kong.

Net fee income slipped 8 per cent year on year to S$637 million, easing from the previous year’s record high as investment banking and loan-related activities moderated amid cautious, risk-off sentiment.

Other non-interest income fell 17 per cent year on year to S$462 million, mainly due to softer trading and investment income.

Total income declined 6 per cent to S$3.42 billion in Q1, from S$3.66 billion in the previous corresponding period.

Management maintained its FY2026 guidance, unchanged from three months ago. The bank continues to expect low single-digit loan growth, a full-year net interest margin of between 1.75 and 1.8 per cent, and high single-digit fee growth.

Guidance for operating cost growth, at low single digits, and credit costs of between 25 and 30 basis points, were also unchanged.

Customer loans rose 4 per cent year on year to S$354 billion in Q1.

On interest margins, Leong said the bank’s house view remains that the US Federal Reserve will cut rates once in 2026, though the relationship between US rates and Singapore rates has “significantly decoupled”.

UOB is “a lot more sensitive” to the Singapore Overnight Rate Average, or Sora, which has more “limited downside”, he noted, adding that the lender remains on track to meet its net interest margin guidance.

Addressing the ongoing Middle East conflict, Wee said that the bank’s direct exposure to the region is “quite insignificant”, with Leong putting Middle East loan exposure at about 2 per cent of the bank’s total loans.

However, the CEO noted that second-order effects from elevated oil and energy prices could weigh more heavily on small and medium-sized enterprises (SMEs), although the bank is still conducting stress tests to assess the potential impact.

On whether UOB may add provisions to guard against the formation of new bad loans, Leong said the bank is continuing to monitor developments closely.

He noted that UOB’s general provision coverage has remained at 1 per cent for three straight quarters, after the lender pre-emptively added more than S$600 million in provisions in the third quarter of FY2025.

UOB’s non-performing loans ratio improved to 1.5 per cent in Q1, from 1.6 per cent in the year-ago period. New non-performing asset formation – largely on real estate exposure in Greater China – fell to S$341 million in the quarter, from S$400 million in the previous corresponding period.

At the briefing, Wee also stressed that the bank would continue supporting its SME customers, after being asked whether UOB would de-risk its SME portfolio.

“In fact, this is the time – especially the SMEs – you have to stand by them,” he said. “This is not the time to de-risk.”

UOB was the second of Singapore’s three local banks to report Q1 results, after DBS released its numbers on Apr 30. OCBC is due to report on Friday.

Shares of UOB rose 0.1 per cent or S$0.05 to close at S$36.70 on Thursday. The counter is up 4.1 per cent in the year to date.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.