Broker's take: CGS-CIMB says Keppel's trough valuation unwarranted, keeps 'add'

Fiona Lam

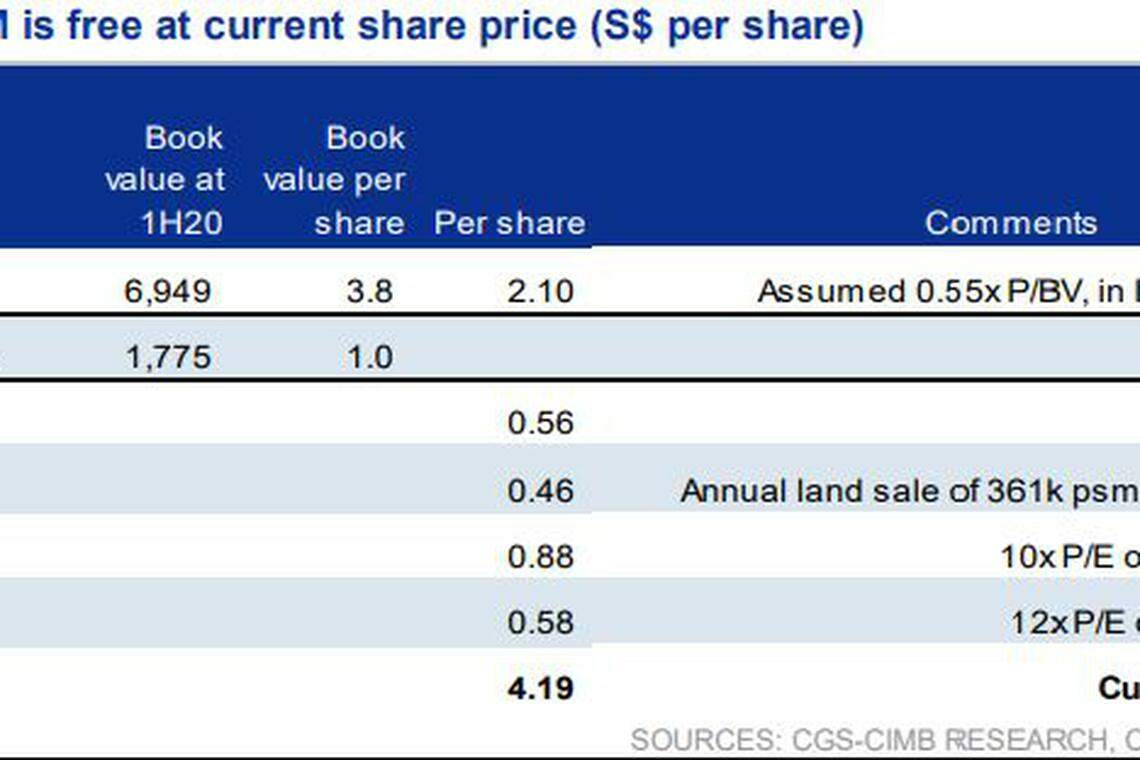

KEPPEL Corp has sunk to a trough valuation that is unwarranted, presenting an opportunity to accumulate the stock now, said CGS-CIMB.

In a report dated Tuesday, the brokerage noted that Keppel's shares were trading at a new trough of 0.7 time price-to-book-value (P/BV) ratio for 2020. The counter had closed at S$4.12 on Tuesday.

That valuation is even lower than during the past oil crisis (0.82 time P/BV in January 2016) and the global financial crisis (1.33 times P/BV in January 2009).

"At the current share price, the market is heavily discounting its offshore and marine (O&M) business to zero value," analyst Lim Siew Khee wrote.

"We think this is unwarranted as the O&M order book of S$3.5 billion (at end-Q2 2020) is in progress and should be able to guide the yard into profitability in 2021."

CGS-CIMB on Tuesday reiterated its "add" call and S$6.46 target price based on sum-of-the-parts valuation.

As at 10.31am on Wednesday, Keppel shares rose S$0.03 or 0.7 per cent to trade at S$4.15.

CGS-CIMB said it has "conservatively factored in" order wins of S$500 million for 2020 and S$1 billion for 2021, below the average order wins of about S$1.9 billion in 2018 and 2019.

The conglomerate on Tuesday announced that its O&M arm had clinched two contracts worth about S$200 million in total. For the US project, the Texas yard will build a high-specification trailing suction hopper dredger, while the Singapore contract is for the conversion of a liquefied natural gas carrier into a floating storage and regasification unit.

These contract wins bring Keppel O&M's orders to S$307 million in the year to date, in line with CGS-CIMB's S$500 million forecast for the full year.

Assuming there is no significant impairment, CGS-CIMB expects Keppel to trade up to its long-term valuation of 12.8 times forward price-to-earnings (P/E) ratio. It is now at about 10.7 times 2021 P/E.

As for Keppel's Singapore yards, Ms Lim said she believes there are fewer than 10,000 staff there at the moment, gradually increasing from the 5,000-strong yard workforce as at the July earnings update, given that the number of new Covid-19 cases in dormitories has been falling.

Keppel's total yard workforce in Singapore had totalled about 24,000 before the country's "circuit breaker", which started in April.

Separately, DBS Equity Research on Wednesday kept its "hold" rating on Keppel, with a S$5.50 target price, implying about 33.5 per cent upside.

DBS noted that the conglomerate's asset management arm is tapping the private education sector.

On Tuesday evening, Keppel Capital said it has raised half of its target commitments for a US$500 million regional real estate investment fund focused on private education assets in the Asia-Pacific.

Decoding Asia newsletter: your guide to navigating Asia in a new global order. Sign up here to get Decoding Asia newsletter. Delivered to your inbox. Free.

Copyright SPH Media. All rights reserved.