HK dividends hold up as China firms stay robust

But Asia-Pac Q3 payout falls 2.8%, pulled down by Taiwan, Australia, while Singapore, South Korea stayed flat

DeeperDive is a beta AI feature. Refer to full articles for the facts.

Singapore

THE slowing global economy seems to be taking its toll in the Asia-Pacific, with lower profits flowing through to lower dividends, according to the Janus Henderson Global Dividend Index, a long-term study into global dividend trends.

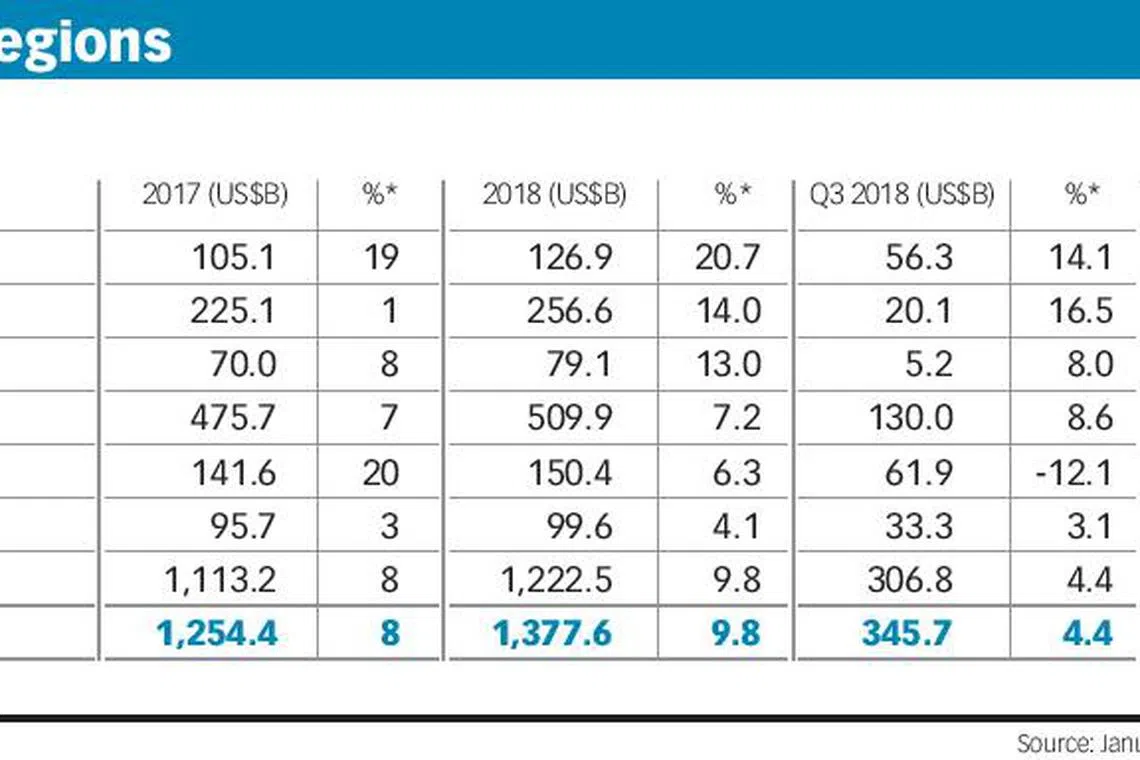

For the third quarter of this year, Asia-Pacific's dividends fell 2.8 per cent year-on-year on a headline basis to US$60.1 billion, the second consecutive quarterly decline.

Weaker exchange rates across the region played a role, but even on an underlying basis (adjusted for movements in exchange rates, among other things), payouts were 1 per cent lower year-on-year.

Within the region, dividend performance in Asia-Pacific ex-Japan was a mixed bag. Australia and Taiwan led the decline; Singapore and South Korea saw flat payouts, while Hong Kong's companies delivered good growth.

The surprising finding for Hong Kong can be explained by the fact that its bourse is home to many mega Chinese companies that continue to perform well despite protracted unrest in the country, said Sat Duhra, co-portfolio manager, Asian dividend Income at Janus Henderson.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

"Sure, that has affected consumer names and more cyclical names, but the real big names in the Hong Kong indices are Chinese firms. They're also not that heavyweight in the index," he said.

Hong Kong's payouts jumped 8.1 per cent on an underlying basis, mainly due to dividends from oil company CNOOC, whose profits rose on rising volumes and good cost control, and from the real estate sector, which grew their payouts by one fifth. Two thirds of companies in its Hong Kong index grew their dividends.

In China, almost half the Chinese companies in the index reduced their payouts, and the modest growth that was achieved was dependent on big increases from just one or two firms.

Chinese dividends totalling US$29.2 billion crept ahead 3.7 per cent year-on-year on an underlying basis and would have been lower without Petrochina's large increase.

In Australia, two fifths of companies in its index cut their payouts. The total dropped 5.5 per cent on a headline basis (or 5.9 per cent lower in underlying terms) to US$18.6 billion, the lowest Q3 total since 2010 in US dollar terms. The biggest impact came from the National Australia Bank, which made its first dividend cut in a decade, as higher costs and rising regulatory pressures meant it had to hold more capital.

Globally, there was also a slowdown in dividend growth, with the trend having begun in the second quarter and continuing into the third. Payouts rose 2.8 per cent on a headline basis to reach a new third-quarter record of US$355.3 billion, equivalent to an underlying growth rate of 5.3 per cent. Mr Duhra said: "After years of strong growth, global uncertainty has been impacting operating performance and kept a lid on previous strong dividend growth, in particular for more cyclical sectors."

He adds that Asian companies as a region have been lagging behind the rest of the world in terms of their dividend payout ratio - at about 35 per cent compared to the rest of the world at 60 to 80 per cent.

"Over the years, because Asian companies have been so conservative, they really built a lot of cash on their balance sheets and so are just generating a lot of free cash flows.

"They have the ability to pay dividends, but not the willingness. But that is changing. Over the last two years, we have seen a big pick-up in dividend payouts across a lot of sectors."

In Singapore, the traditional favourite defensive sectors have tended to be real estate investment trusts (Reits), banks and telcos; made more attractive by lower-for-longer interest rates that increase the spread between equity and bond yields.

Gazing into its crystal ball, Janus Henderson has left its US$1.43 trillion forecast for global dividends unchanged for 2019. This represents a headline increase of 3.9 per cent, or underlying growth of 5.4 per cent.

"It is likely that dividend growth next year will slow further. Consensus expectations for corporate earnings still seem too high, given the current slowdown in the global economy; slower profit growth will impact dividends too,"it said.

Mr Duhra adds that amid the geopolitical uncertainties in many countries, the preference for companies is still to hold cash for a rainy day. But as for Singapore, he thinks the defensive stocks will maintain steady operational performances and dividend payments.

"I don't see any risks around Reits, telcos, or banks cutting their dividends. In fact, the banks especially have done a very good job increasing them over the last couple of years."

Copyright SPH Media. All rights reserved.

TRENDING NOW

Shelving S$5 billion office redevelopment plan proved ‘wise’ as geopolitical risks mount: OCBC chairman

Eurokars Group introduces rental car franchises Enterprise Rent-A-Car, National Car Rental, and Alamo to Singapore

20 photos that show how dramatically Singapore has changed in two decades

Singapore’s key exports up 15.3% in March from electronics surge, exceeding forecasts