Re-train, not retrench, when jobs are at risk, financial sector told

Ong Ye Kung says Singapore aiming for annual 4.3 per cent growth for the sector, with productivity fuelling over half of the growth

DeeperDive is a beta AI feature. Refer to full articles for the facts.

Singapore

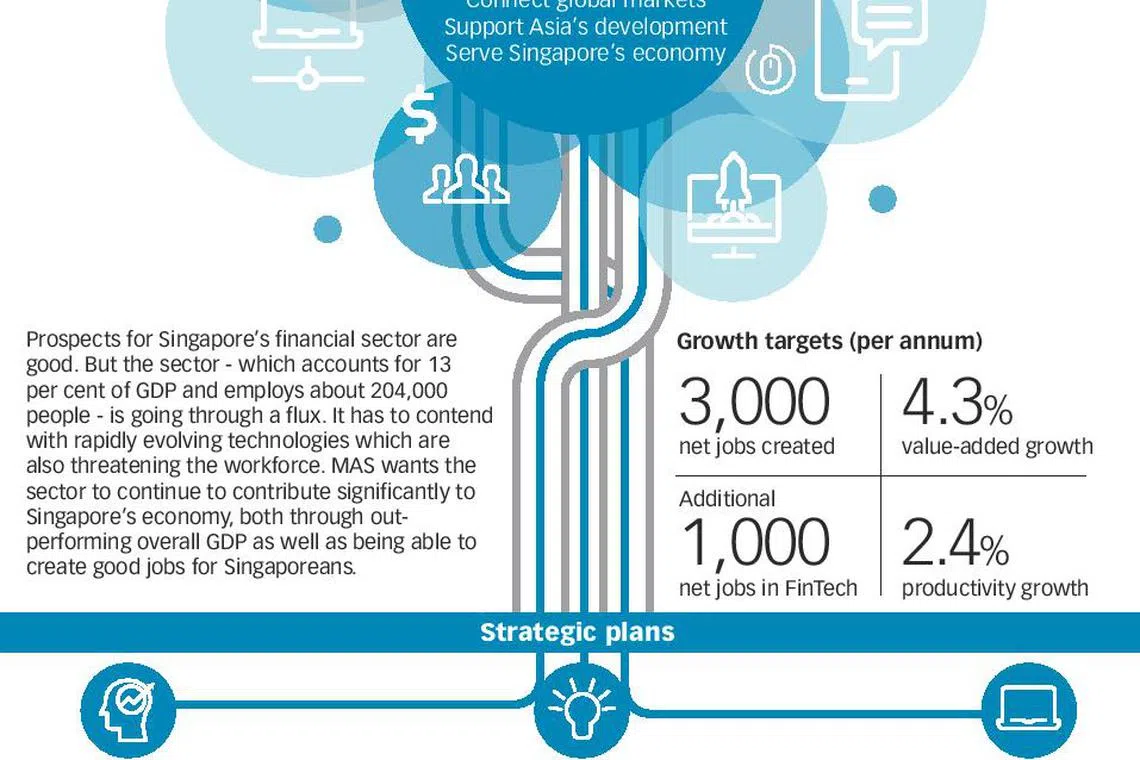

SINGAPORE'S financial sector has put out an ambitious target to continue outpacing the overall economy in growth terms - a target that also aims to take as many financial professionals along the journey as it can while managing job displacements ahead.

The sector aims to create 3,000 net jobs in financial services every year, as well as an additional 1,000 net jobs in the fintech sector annually. But with the digital disruption, the Singapore government is also sending a signal that financial institutions should not be too trigger-happy in firing their staff.

Speaking at the launch of the financial services industry transformation map (ITM), Ong Ye Kung, Minister for Education (Higher Education and Skills) and board member of the Monetary Authority of Singapore (MAS), said Singapore must be able to help the less-skilled and vulnerable keep up with the changes and stay relevant.

"When an existing activity is disrupted and jobs become at risk, the tendency is to lay off staff. But this cannot be the solution of first resort."

He said the sector's ITM expects financial services' GDP to grow at 4.3 per cent per annum on a real value-added basis over the medium term, nearly twice as fast as the overall economy. Over half, or 2.4 per cent of the growth, will be driven by productivity.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

The hope is for Singapore to be a top financial centre in Asia that is more deeply plugged into global markets, drawing more capital into Singapore by building expertise here in emerging, specialised areas such as pricing insurance for natural disasters, creating efficient forex pricing, and matching up financing for infrastructure projects.

Mr Ong said the growth figures are "ambitious", given the significant changes happening in the industry.

"But we are determined to be net gainers in this era of change." Both growth figures and productivity rates are above what is expected for the overall economy. Singapore's economic growth in 2017 is expected to be between 2 per cent and 3 per cent, and productivity rose by just one per cent last year, after several years of negligible growth.

This comes as technology has offered much promise in speeding up many processes in the financial services segment. But the projections also come amid rising questions about jobs with the advent of technology. For example, as banks try to meet the rising compliance burden, they have at this point been hiring a large number of compliance staff to meet the demands. Banks are also investing in technology to automate processes in this area.

The MAS said it will strengthen human-resources practices on hiring and redeployment. This will include ensuring a sustainable mix of both foreign and local talents.

It added that it will continue to work with financial institutions, tripartite partners, polytechnics and universities, to build a local pipeline of specialised talent, particularly in information technology. MAS will also work to reskill and redeploy professionals into job growth areas through professional conversion programmes.

Mr Ong added: "How do we address the challenge of talent and skills? The answer cannot be poaching - widely practised in the industry, but is not the long-term solution.

"We simply have to expand and deepen the talent pool. And we need to do this at a pace that can catch up with the rate of digitisation and automation which are re-defining job roles, "

Banks tell The Business Times that efforts have been underway to build the talent pipeline. OCBC said the average number of man-days of training per employee in 2016 was 7.8 days, well above the target of 5 days.

DBS pointed to its announcement in August to invest S$20 million over five years to re-skill employees to have them ready for the digital workforce. It has also collaborated with the IMDA (Info-communications Media Development Authority) to introduce the industry's first fintech training programme to young professionals in technology skills.

UOB has also in the first nine months of this year almost doubled its number of data scientists and analysts as part of a focus on understanding and anticipating customer behaviour. It invested almost S$20 million in training programmes last year, with employees putting in an average of 37 hours in training.

Not to be outdone, Citi Singapore said it has beefed up an internal leadership programme to incorporate potential job exchange across business franchises, functions, and competencies. In the 2017-2018 edition of this leadership programme, 73 per cent of participants were Singapore citizens or permanent residents. This is up from 59 per cent a year ago.

It has also sponsored nine Singaporean leaders including Han Kwee Juan, CEO of Citibank Singapore, to take part in the MAS's Asian Financial Leaders Scheme.

Over at Standard Chartered Singapore, it has seen a 10 percentage point increase in the share of jobs in Singapore going to Singaporeans.

The talent development drive also extends to the private banking segment, as Singapore moves to develop itself into a leading international wealth management hub that offers comprehensive and high-quality wealth advisory services.

Bank of Singapore has put serious dollars to work, investing more than US$30 million in skills development, said its CEO Bahren Shaari.

Citi Private Bank meanwhile has offered customised career development for its private bankers, with most of its senior private bankers having been with the bank for at least 15 years.

Every year, a few thousand employees go through the Credit Suisse Wealth Institute, set up in Singapore.

And at UBS, it has a Youth Finance Academy, which gives pre-tertiary students exposure to the depth and breadth of career opportunities in the finance industry, said Edmund Koh, head of wealth management in Asia Pacific, at UBS.

READ MORE:

Copyright SPH Media. All rights reserved.