Poison pen letters can doom IPOs but Singapore's record is sparse

Only 5 IPO-aspirants have been sunk in the 14 years since the adoption of a public-scrutiny process in the local framework

Singapore

THE mighty pen is rarely deadlier than in an initial public offering (IPO), when one poisoned nib can fell a multimillion-dollar deal.

But the dreaded poison pen has killed late-stage IPOs only a handful of times in the 14 years since the adoption of a public-scrutiny process in Singapore's IPO framework.

Industry players add that the market here has become more adept in anticipating issues and separating the wheat from the chaff.

Drew & Napier deputy managing director of corporate and finance Sin Boon Ann said: "The system is a lot more mature."

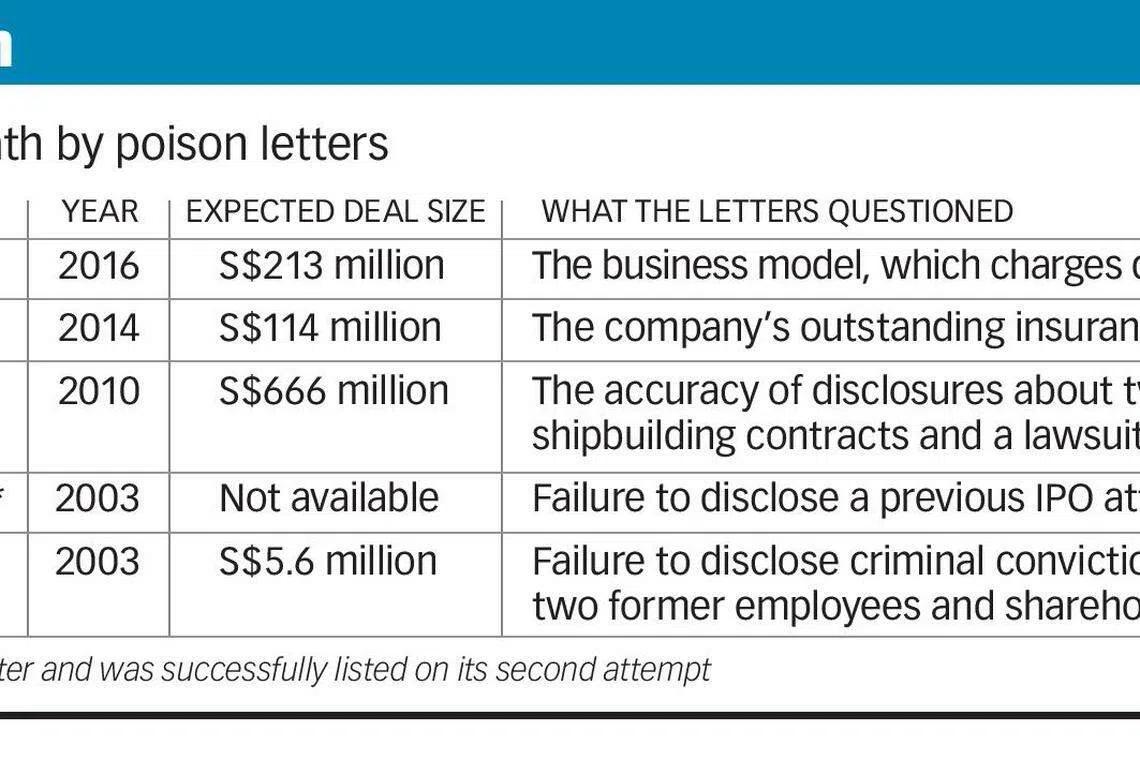

Nevertheless, a poison-pen letter has sunk managed-care provider Fullerton Healthcare's plan to list; the company said this week that it has shelved its IPO plans amid market uncertainty.

Navigate Asia in

a new global order

Get the insights delivered to your inbox.

The IPO, which had been expected to raise about S$213 million, was abruptly pulled in October after a poison-pen letter raised questions about the company's business model.

Speaking to The Business Times this week, Fullerton chief financial officer Ramesh Rajentheran said all the issues raised could be "easily answered by the company". As for the business model, he said that Fullerton is consulting with healthcare providers to explore alternatives.

Fullerton is not the first late-stage IPO to suffer a fatal prick of a poison pen.

A check of news archives going back to 2002 turned up only five cancelled deals directly attributed to poison pens.

That year, Singapore introduced a "public-exposure" period for IPOs. Anyone can submit a comment to the regulators at any time during the IPO process, but it is during this public-exposure period lasting at least two weeks that the listing aspirant is most exposed, with an almost-complete version of its prospectus revealing to the world what the company believes to be an accurate report of all the material information about the business. Any allegation that seems sufficiently material must be addressed.

Wong Partnership deputy chairwoman Rachel Eng said: "The current system places the company seeking a listing in a vulnerable position.

"Whenever a poison pen is received, the regulators feel there is a need to investigate."

She noted, however, that most such letters are frivolous, and not all deals receive such letters.

"For example, it could be an anonymous letter that simply states 'The profits of this company are fake'. The regulators take each poison pen letter seriously and will require the company and its advisers to provide sufficient explanation before permitting the company to continue with the IPO process."

It is the unhappy former insider that strikes the most fear.

Said Mr Sin: "Disgruntled former accounts personnel with intimate knowledge of the company's financial information and business practices can potentially do significant harm to the issuer through poison-pen letters."

There were more poison-pen letters in the early days than now, he noted, and attributed this partly to better screening by regulators and IPO advisers, as well as to a more discerning public, especially when it comes to using anonymity.

For him, the problem with anonymity is less about holding an accuser accountable, and more about whether the company can ascertain whether an allegation is founded.

"Where's the issue of transparency? It's your document and you have to be responsible and reliable. You have to disclose every piece of material information," he said.

After all, a poisonous allegation is better discovered sooner than later, when questions of professional negligence could be raised.

Mr Sin said: "The way to improve the process is to have better guidance to the public on what to feed back, by indicating more precisely the issues that the regulators would be concerned with, the kind of information required, and what would be considered a frivolous complaint."

He added that non-anonymous submission through a secure framework could also be encouraged, to allow for a more thorough investigation.

Singapore Exchange (SGX) chief regulatory officer Tan Boon Gin said the regulator employs a test of materiality and proof: "We will consider carefully the information received and work with the issue manager and company to resolve any material issue raised and to ensure disclosures in the prospectus are not false and misleading.

"However, we will not entertain feedback that is clearly frivolous or vexatious."

For IPO advisers, who are professionally obliged to ensure that IPO candidates disclose all material information accurately, the best solution is prevention and anticipation. This means doing stringent due-diligence and advising clients to bare all.

Jack Kang, head of equity capital markets at United Overseas Bank, said: "As a sponsor and issue manager, UOB places great emphasis on the importance of complete disclosure and will advise the IPO candidate to disclose all matters or issues that could potentially raise concerns.

"Together with other professional parties, including the lawyers and auditors, we will deliberate such matters or issues and resolve them before making an IPO application to the exchange. These matters or issues, including the method of resolution, will also be highlighted to the exchange for their attention."

Of course, all that preparation will not stop someone from lodging a complaint if they have an axe to grind , so this is where some life skills come in.

Mr Sin said: "The practical side of things is, try to make peace and don't make enemies."

Copyright SPH Media. All rights reserved.